As part of the recent Optimism Retroactive Public Goods funding program – there was a discussion that startups with large amounts of venture funding shouldn’t apply

This isn’t the first time a discussion like this has happened – and I think broadly reflects push back in public governance related to paying commercial entities large fees related to software and services they want to provide to protocol communities

With roles as both a generalist venture capital investor (who invests in crypto) and an enthusiast for the potential of DAOs as a new social technology – I want to make the argument that rather than discourage these companies – we should encourage this activity – and even more – figure out ways to make it easier for companies selling software and services – to sell into and support DAOs as customers

1.

While companies in new industries often start vertically integrated – over time, as markets mature – early entrants in the market benefit from new suppliers and ecosystem participants entering to provide software and services across multiple players

Rather than need to build every component of their system, the company can focus on the key features that they’re best at – and benefit from the competition from other new entrants competing to support them – as well as the shared learnings those companies receive from working across multiple customers

2.

In the software industry, one example of this is related to IT spend – software companies could develop all of the software they need to run their own business – but rather than do that – they often buy software from other commercial vendors that focus on the specific problem to be solved – this report from 2020 shared that IT spend by software companies was almost 25% of the customer’s spend by revenue

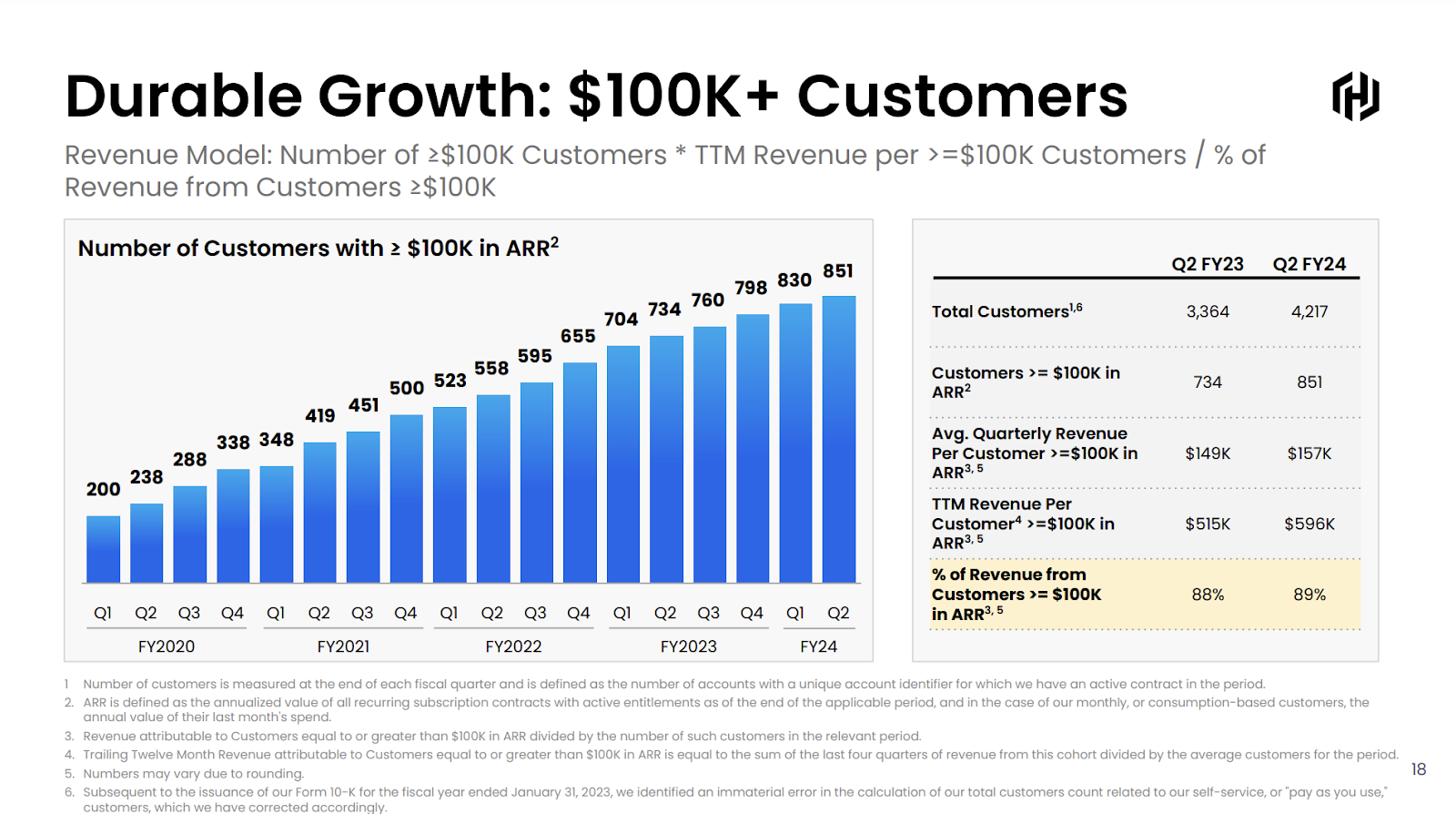

And by company – some of these deals can be quite large – as one example – HashiCorp disclosed having over 800 customers spending more than $100k per year with them (and had previously disclosed that they have one customer who spends more than $10 million a year with them)

3.

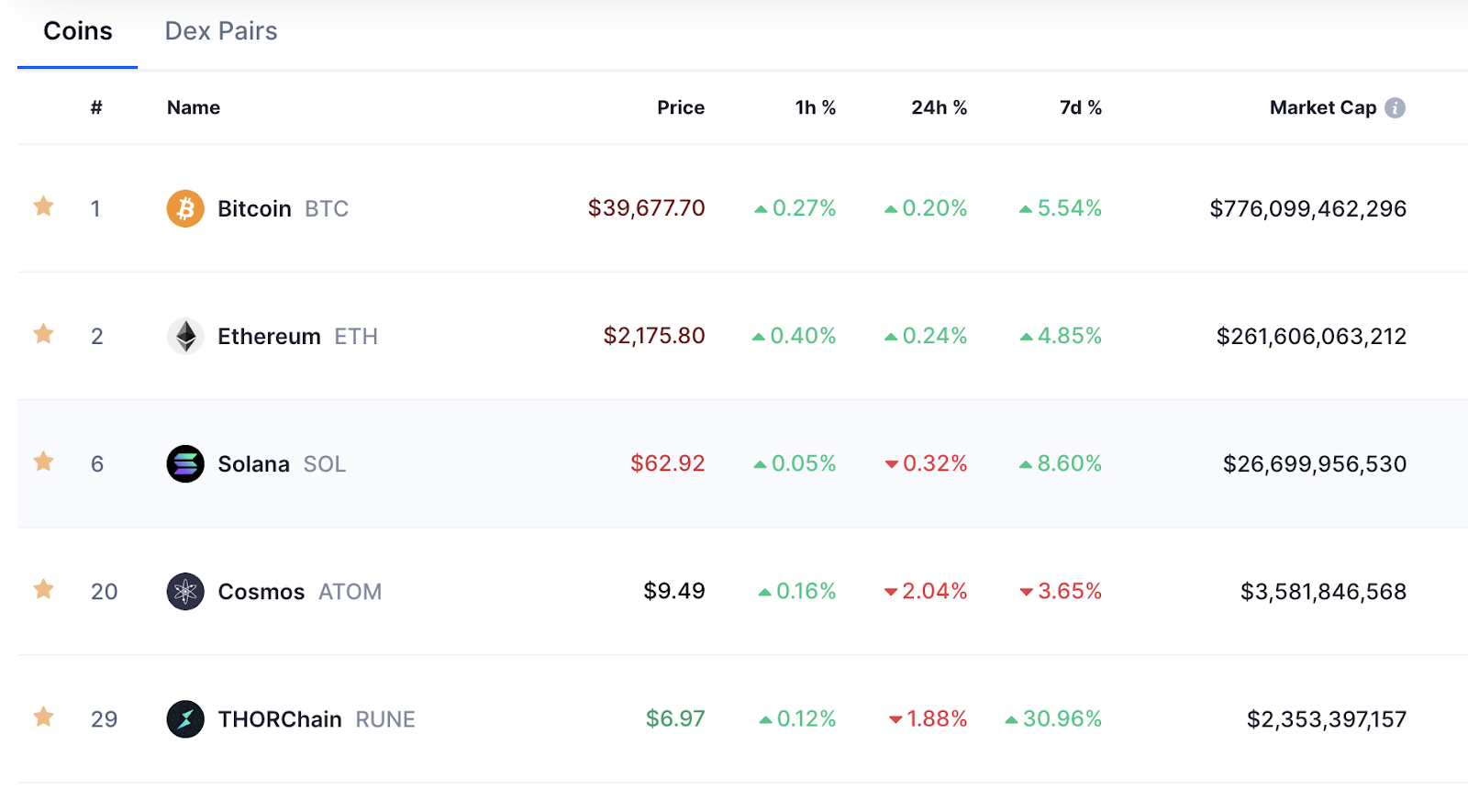

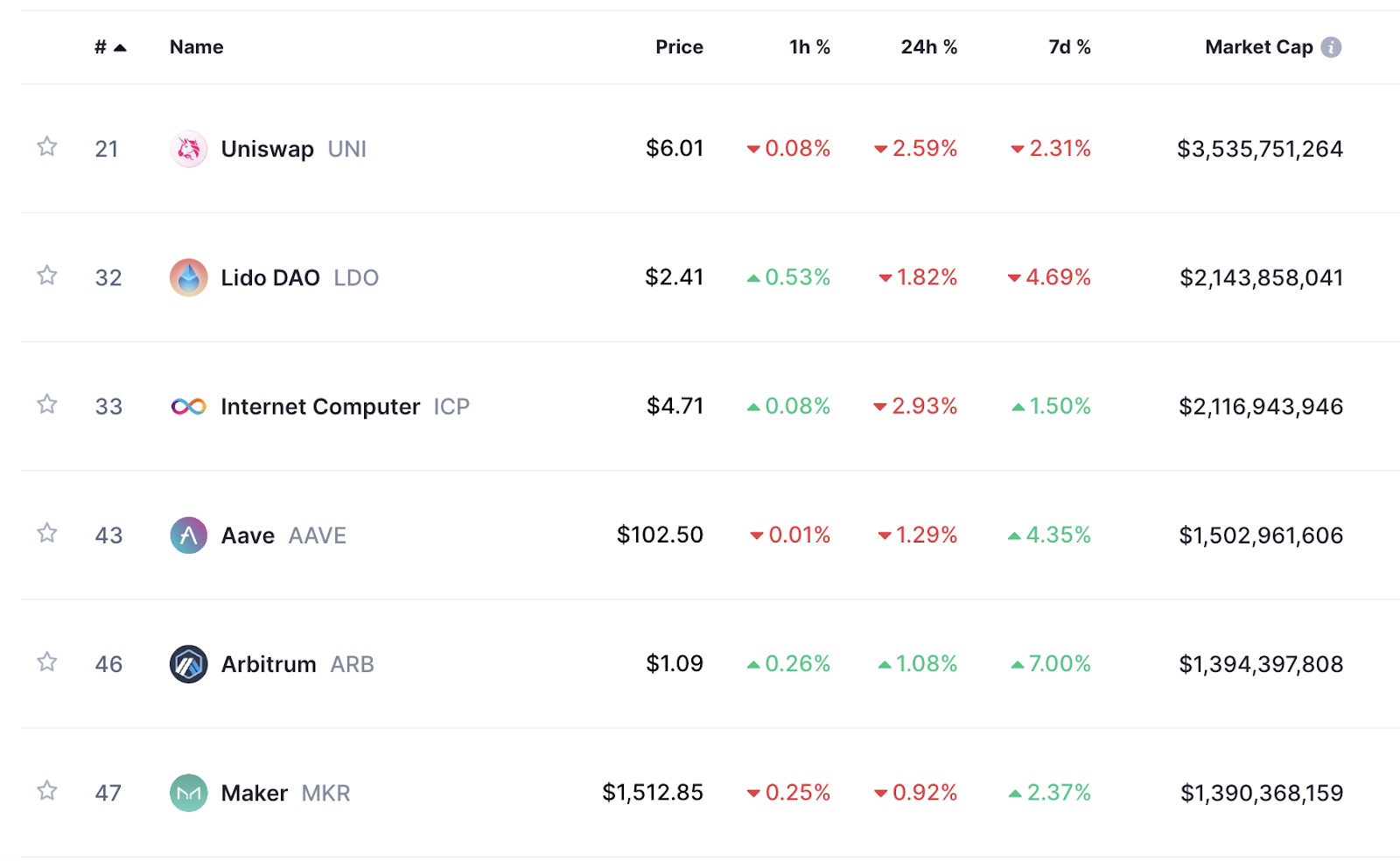

I think of the broadest definition of DAOs, which I’d argue is uses blockchain as a social technology – which uses the economic incentives of the network to drive user behavior (which would include L1 blockchains like Bitcoin, Ethereum, and THORchain) as well as the more narrow definition of DAOs (where token holders may be able to vote and participate in governance – including projects like Yearn Finance, Autonolous, and Hair DAO)

Under either of these definitions – these ecosystems are large:

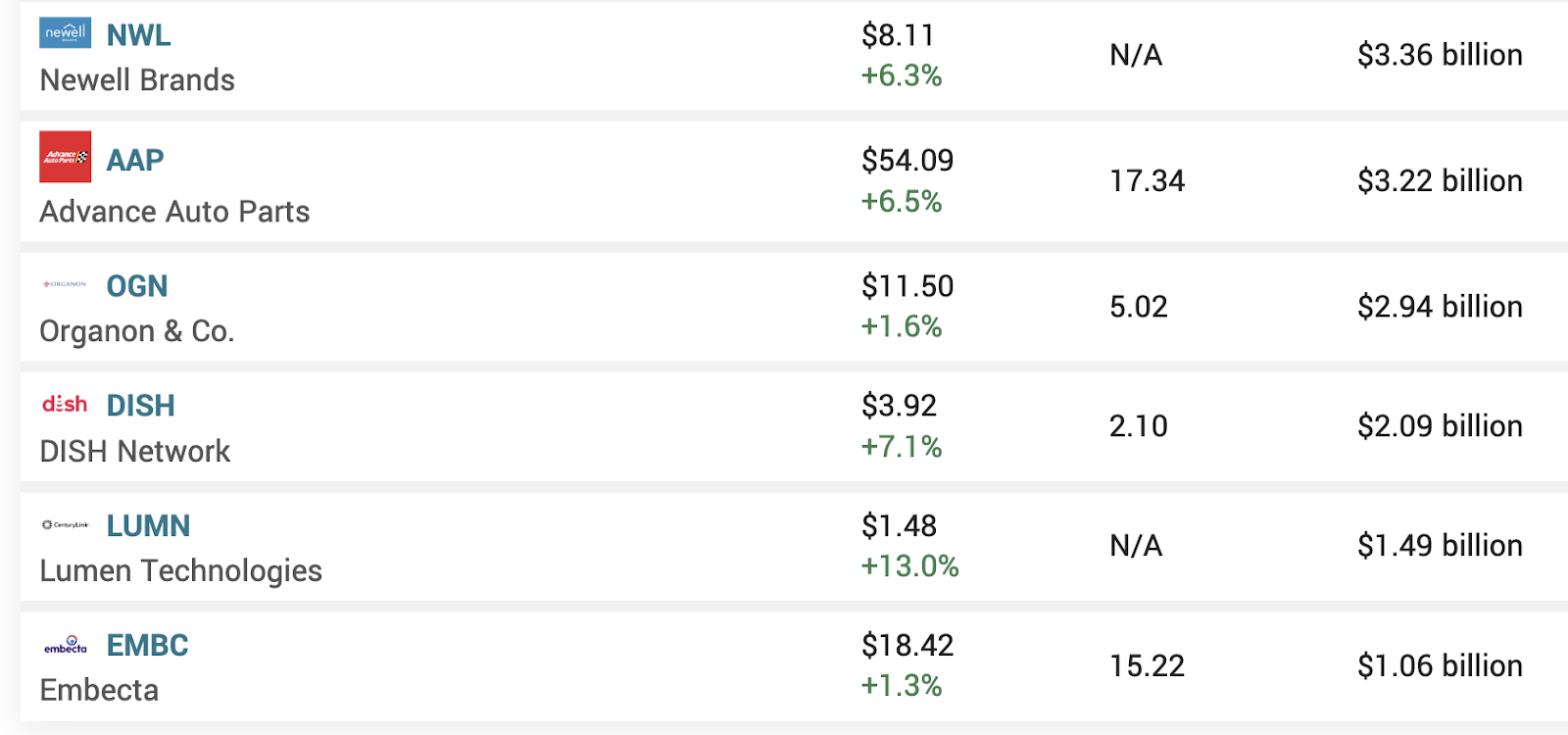

And are the size (or larger) of companies included in the S&P 500 index (bottom of the list here):

4.

So while DAOs should continue to support small open source projects and internal teams – if we want the industry to mature – I’d argue that we want to support companies building software and services to support the growth of these ecosystems

A.

I think we want more founders starting companies to sell software and services into these ecosystems – to support projects themselves and developers building on top

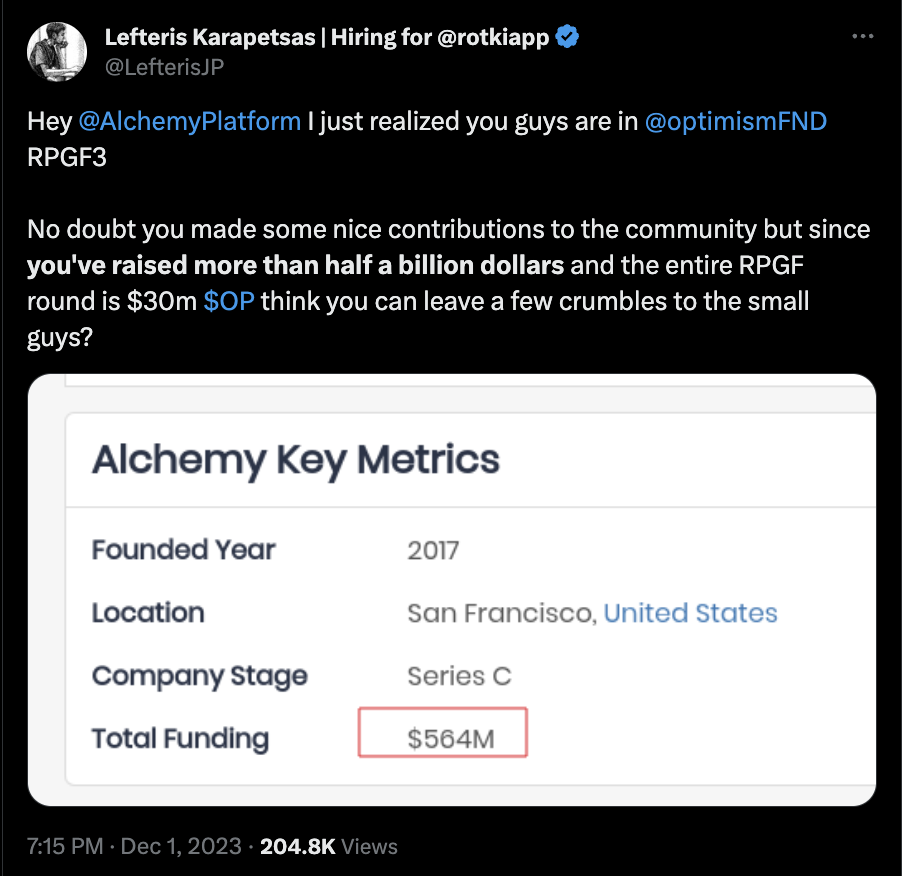

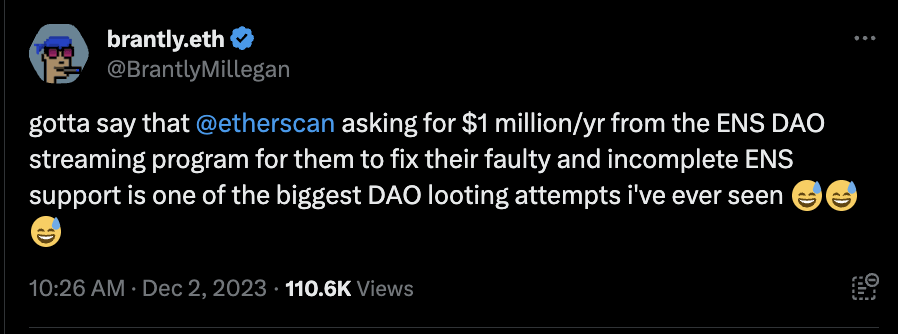

If startups like Etherscan, Gauntlet, Coordinape, and Flipside Crypto are successful selling software into these ecosystems (and as such building valuable businesses) – more individuals will think about starting companies to sell into DAOs – bringing in more competition and better offerings for DAOs

B.

The opposite is also true – if the only way to generate new economic value is by launching a new protocol (or selling into centralized foundations) – founders will only focus there – which I think ultimately will make it harder + take longer for these ecosystems to be successful

C.

As a VC investor – I realize that my opinion is incredibly biased – but I also think we’re all collectively aligned – I think more startups building software + services to sell into DAOs are successful – it will increase the likelihood and speed of DAOs (both layer one blockchains and projects building on top of those ecosystems) being successful

(And – I’d argue for new emerging ecosystems that are competing for developers (eg L2s) or new applications competing for users – the ability to effectively use outside software and services – may become a competitive advantage – allowing them to grow more quickly and effectively than their competitors)

D.

But – what I’m most excited about is what happens next – once we get comfortable with DAOs purchasing large software contracts – we get to experiment with innovative new, DAO-native business models

(As a related plug – please check out Community Enabled Analytics from Flipside Crypto – which uses yield from token delegations to support new user acquisition and retention for its protocol customers.

I’m biased, but think this program has the ability to help base layer protocols and decentralized projects drive their business goals – but has been criticized in similar public commentary)

5.

If you liked this content, you may also like my post on “The Symbiotic Relationship Between Corporations and DAOs” or my post on “How Blockchain Infrastructure Is Unlocking Economic Value”

True (nor I) are an investor in Alchemy or Gauntlet – True (or I) may be an investor in all of the other crypto protocols and startups mentioned by me in this post